Best Colorado Refinance Rates in 2026: What Homeowners Need to Know Right Now

If you own a home in Colorado and have been watching interest rates closely, 2026 is shaping up to be one of the most important years for refinancing decisions in recent memory. Rates are moving, forecasts are shifting, and the window of opportunity may be narrowing. Here is everything you need to know about the best Colorado refinance rates in 2026 and how to position yourself to take full advantage.

Where Colorado Refinance Rates Stand Today

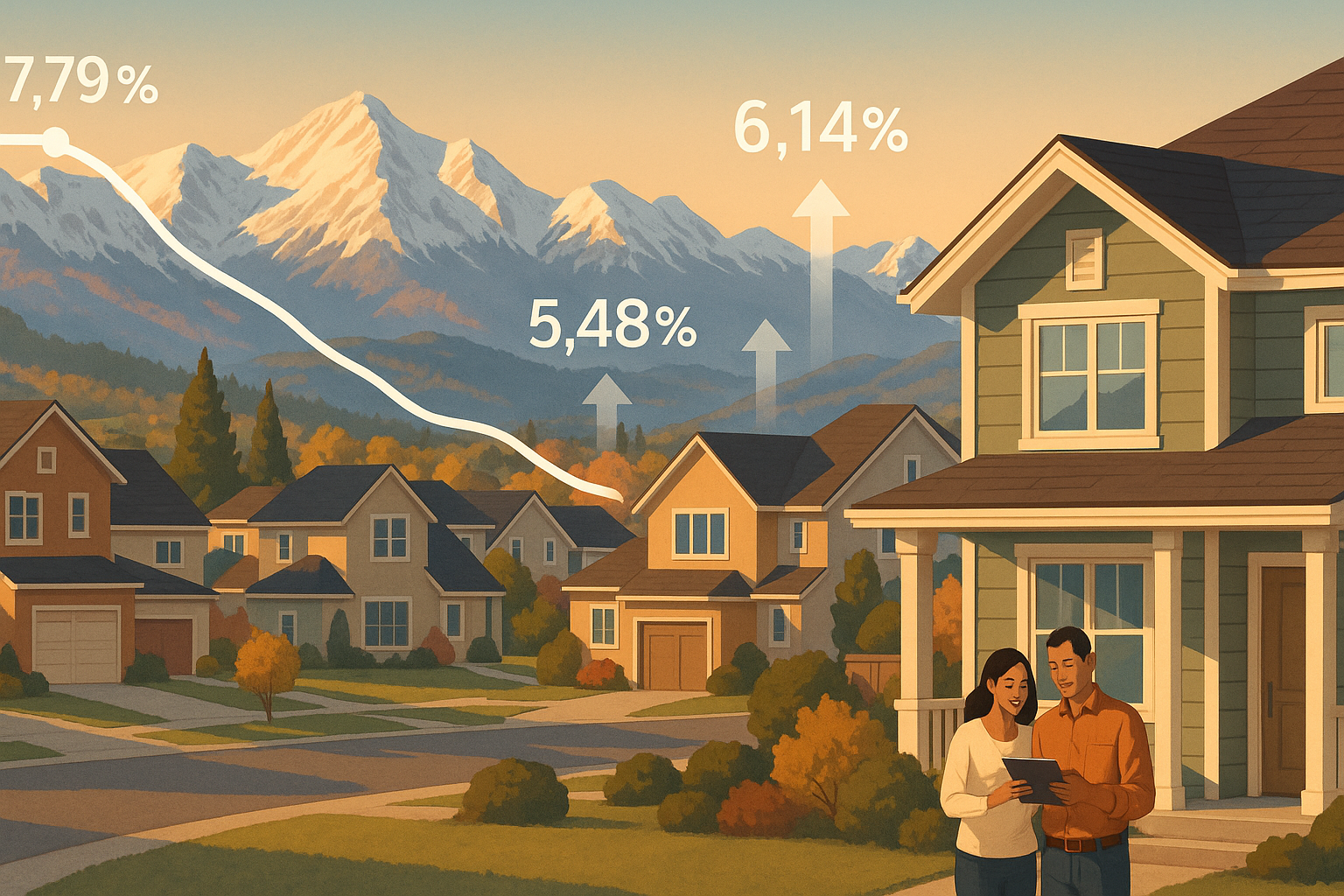

As of March 19, 2026, current interest rates in Colorado are 6.14% for a 30-year fixed mortgage and 5.48% for a 15-year fixed mortgage. These figures sit slightly below the national average. The national average 30-year fixed mortgage APR is 6.41%, and the national average 30-year fixed refinance APR is 6.70%, according to Bankrate's latest survey of the nation's largest mortgage lenders.

For Colorado homeowners, that gap between state and national averages is meaningful. It means qualifying borrowers in the Centennial State may be able to secure more competitive terms than their counterparts in other parts of the country.

In line with national trends, mortgage rates in Colorado have been gradually stabilizing. That stabilization follows a turbulent stretch that saw rates climb dramatically from pandemic-era lows. A combination of six Federal Reserve rate cuts totaling 1.75%, cooling inflation, and declining Treasury yields have slowly brought rates down from the painful peak of 7.79% reached in October 2023.

Are Interest Rates Going Down in 2026?

The short answer: yes, modestly, and with some caveats.

Mortgage rates are expected to gradually decline in 2026 as inflation cools and the Federal Reserve considers rate cuts. However, the pace and extent of these drops will depend on broader economic conditions, including labor market trends and potential recession risks.

Several major institutions have weighed in with their forecasts:

- Fannie Mae's February Housing Forecast predicts that 30-year fixed mortgage rates will average 6.1% in the first quarter of 2026, down meaningfully from 6.8% earlier in 2025.

- The Mortgage Bankers Association predicts that 30-year mortgage rates will hold at 6.1% through most of 2026.

- Redfin and Realtor.com both predict rates to average around 6.3% in 2026, while Bright MLS forecasts an average of 6.15% by year-end.

- Morgan Stanley strategists forecast that a decline in the benchmark 10-year Treasury yield to about 3.75% by mid-2026 could help lower the 30-year fixed mortgage rate to around 5.50% to 5.75%; however, the strategists expect mortgage rates to then rise again in the second half of 2026 and in 2027.

Fannie Mae's expectations for slower GDP growth indicate a weaker economy in the next couple of years, and in this case, mortgage rates would go down. Additionally, the 30-year fixed mortgage rate follows the 10-year Treasury yield more closely than any other index, so a lower yield would likely translate to home loan rate decreases.

One thing experts agree on: do not hold out for a return to pandemic-era rates. Many economists agree that if inflation remains under control, we may see mortgage rates gradually come down by 2026, but it is unlikely we will return to the historic lows of 2020 to 2021 in the short term.

What This Means for Colorado Refinancers

If you locked in a mortgage at a higher rate over the past two years, the current environment deserves your attention. If you locked in a mortgage at 6.5% or higher in the past two years, 2026 could be your window to refinance.

Lower mortgage rates can benefit homeowners, homebuyers, and home sellers. Homeowners may have the opportunity to refinance their existing mortgages, helping to reduce monthly payments, shorten loan terms, or even tap into home equity.

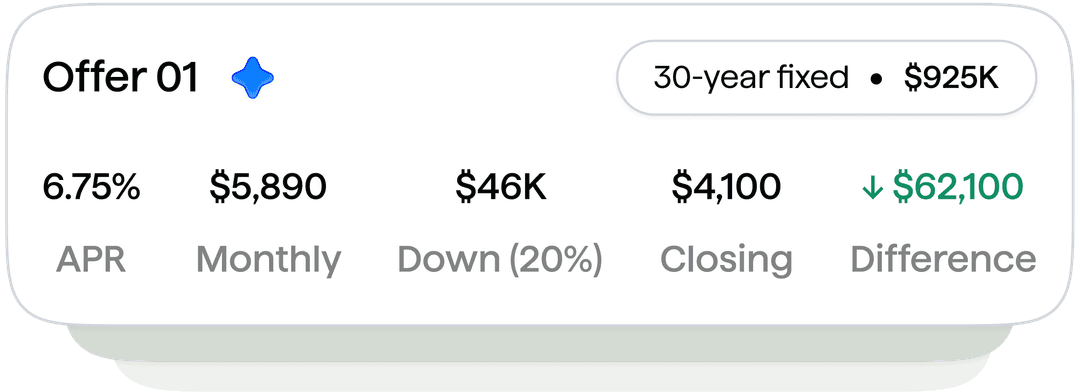

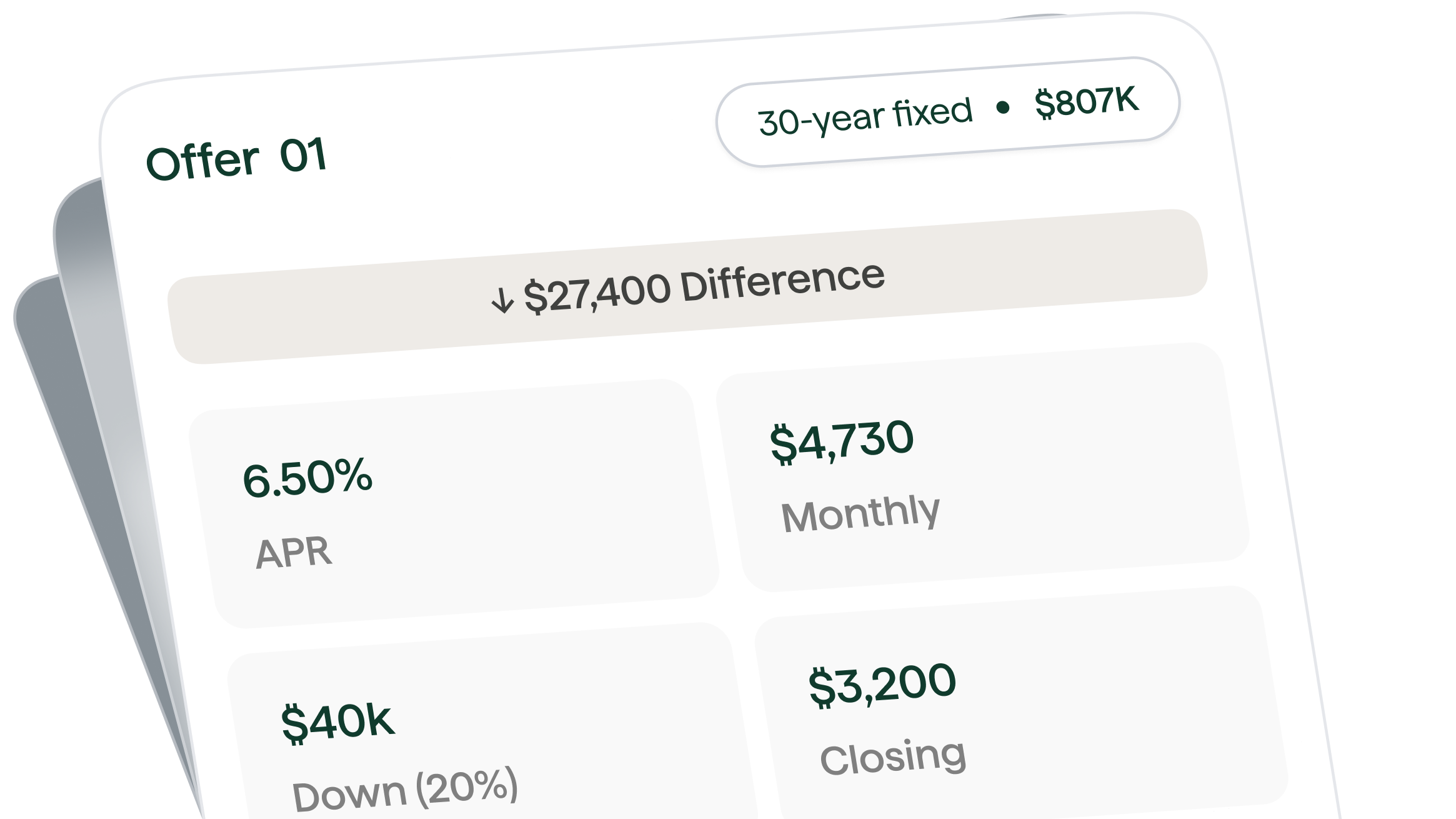

Even a small rate reduction can produce real savings. A drop of even 0.5% in your interest rate can lower your monthly payment and reduce the total interest you pay over time. And for a $1 million home, the monthly cost today could be $4,900 at a rate of 6.20%, versus $4,542 at 5.50%, a difference of roughly $358 per month.

Colorado homeowners also have two primary refinance paths to consider:

- Rate-and-Term Refinance: This is a simple and common refinance that replaces your existing mortgage with a new one. That could mean refinancing from an FHA to a conventional loan to remove FHA mortgage insurance if you qualify, or refinancing a conventional loan to lower your rate or shorten your payoff timeline.

- Cash-Out Refinance: This refinance replaces your existing mortgage with a new, larger one and lets you take a portion of your equity out as cash. The amount you can access depends on your home value, how much you still owe, lender loan-to-value limits, and closing costs.

How to Get the Best Colorado Refinance Rate

Knowing that rates are trending down is only half the battle. Securing the best possible rate requires preparation on your end. Here are the key steps:

1. Shop Multiple LendersTo secure the best mortgage and refinance rates in Colorado, it is a good idea to shop around and compare offers from at least three lenders. Rates and fees can vary significantly from one institution to the next.

2. Compare APR, Not Just Interest RateTo get the best refinance rate in Colorado, work on improving your credit score. It also pays to carefully compare APRs, which include the interest rate and the associated fees, to ensure the best value.

3. Strengthen Your Credit ProfileCredit score has a major impact on your mortgage rates, with higher credit scores generally meaning lower interest rates. Your credit score is not the only thing that affects your mortgage rate, however. Your down payment, debt-to-income ratio, loan term, and other factors will also affect your rate.

4. Calculate Your Break-Even PointBefore refinancing, consider the upfront costs, long-term costs, and how long it will take to break even. Also keep in mind that refinancing into a new, longer-term loan may ultimately cost you more overall.

5. Track Rates ConsistentlyCheck Colorado refinance rates daily to capitalize on the best refinancing opportunity. Rate movements can be swift, and timing matters.

6. Consider a Rate LockRate locks are made between you and your lender, guaranteeing a specific interest rate, even if the market goes up, over a set period of time. This protection can help give borrowers peace of mind, with most rate locks lasting between 15 and 60 days.

The Colorado Housing Market Context

Understanding the broader market helps frame your refinancing decision. The median single-family home sale price in Colorado was $580,000 in October 2025, according to the Colorado Association of Realtors. That sustained high price, plus today's higher mortgage rate environment, could make housing affordability a challenge for some buyers, depending on where you are looking.

Colorado mortgage rates are significantly impacted by the health of the real estate market. The demand for houses, regional real estate values, and overall economic conditions are some of the variables influencing Colorado's current mortgage rates.

On the national outlook, most forecasters expect rates to hover in the low 6% range through mid-year, with potential for one or two additional Fed cuts later if inflation continues cooling or the labor market weakens further.

The Bottom Line

Colorado homeowners are sitting at a pivotal moment. Rates have come down from their peak, forecasts point to continued, if modest, declines through at least mid-2026, and the refinancing calculus is becoming more favorable for those who locked in at higher rates. Refinancing your mortgage involves applying for a new mortgage and using the funds to pay off your existing loan. Refinancing could lead to significant savings, especially if mortgage rates have dropped or your credit has improved since you took out your loan.

The key is not to wait for the perfect rate that may never arrive. Instead, run the numbers on your current loan, compare offers from multiple lenders, and make a decision rooted in your personal financial timeline. If the math works today, waiting for a slightly lower rate tomorrow is a gamble that may not pay off.

Ready to see what your Texas refinance rate looks like today? Check your rate with Ralo now.

Related Articles

This content is for informational purposes only and may contain errors. Please contact us to verify important details.