Best Refinance Rates in Texas (2026): Is Now the Right Time to Pull the Trigger?

Texas homeowners, the rate environment is shifting beneath your feet, and the decisions you make in the next few months could affect your finances for years to come. Whether you locked in a mortgage near the 2023 peak or you are sitting on a loan that no longer fits your life, here is a ground-level look at where Texas refinance rates stand right now, where they are headed, and how to position yourself to win.

")

The Numbers on the Ground: Texas Rates Right Now

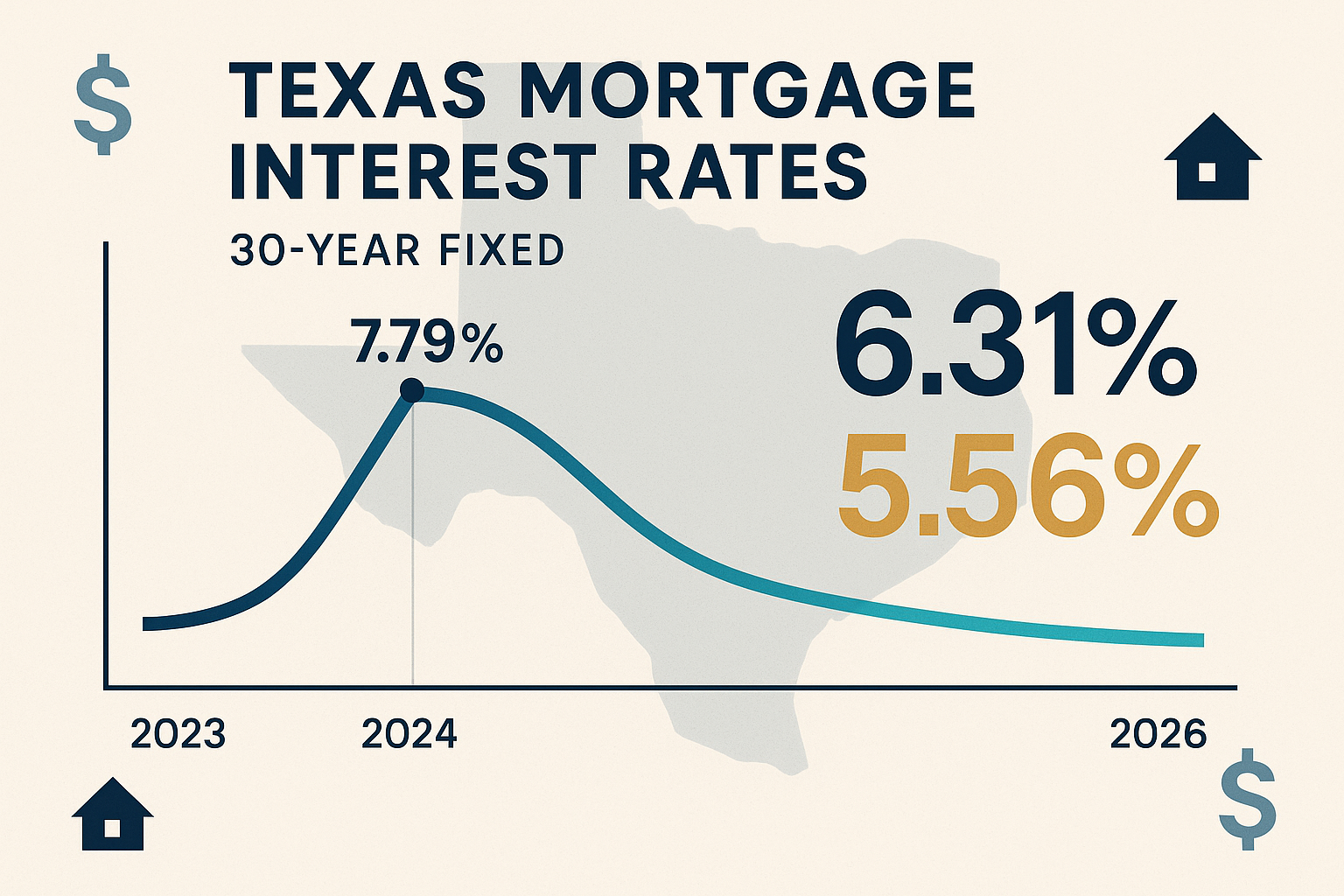

As of March 19, 2026, current interest rates in Texas are 6.31% for a 30-year fixed mortgage and 5.56% for a 15-year fixed mortgage. Compare that to the national average 30-year fixed mortgage APR of 6.41% and the national average 30-year fixed refinance APR of 6.70%, according to Bankrate's latest survey of the nation's largest mortgage lenders.

That spread matters. Texas borrowers with strong credit profiles are finding rates that sit meaningfully below the national benchmark, which means the Lone Star State is quietly one of the more competitive refinance markets in the country right now.

At one of their highest points, in October 2023, 30-year fixed rates climbed to 7.79%, which pushed millions of would-be buyers out of the market. Since then, a combination of six Federal Reserve rate cuts totaling 1.75%, cooling inflation, and declining Treasury yields have slowly brought rates down. As of late February 2026, it is possible to secure a 30-year rate under 6% for qualified borrowers.

If you bought your home in Texas when rates peaked near 8% in the fall of 2023, refinancing now could save you money.

Breaking News: What the Fed Just Decided and What It Means for You

The Federal Reserve met on March 18, 2026, and the outcome is directly relevant to every Texas homeowner watching rates.

The Federal Reserve left interest rates unchanged amid mounting uncertainty over how the Iran war will impact the economy, raising questions over whether any rate cuts will occur this year. The Fed's monetary policy panel voted 11-1 to leave the benchmark federal funds rate unchanged at a range of 3.5% to 3.75%.

It marked the second straight meeting with rates being held steady after three successive 25-basis-point cuts in September, October, and December to end last year.

Despite the pause, the door to cuts is not fully closed. Despite the elevated uncertainty, officials again signaled they still expect a few rate cuts ahead. The closely watched "dot plot," which reflects individual members' rate projections, pointed to one reduction this year and another in 2027.

Chicago Fed President Austan Goolsbee said additional rate cuts are possible this year if inflation eases. Fed Governor Stephen Miran called for four quarter-point cuts in 2026 to support the labor market and stimulate productivity.

The caution, however, is real. Soaring oil and gas prices, sparked by the conflict in the Middle East, now have economists tearing up their forecasts. Higher energy prices could ripple through the economy, pushing up transportation costs, food prices, and utilities.

Where Mortgage Rates Are Headed: The 2026 Forecast Picture

Despite the near-term uncertainty, the longer arc of rate forecasts still points downward. Here is what major institutions are projecting:

Fannie Mae's March Housing Forecast predicted that the average 30-year fixed mortgage rate will remain at 6% in Q1, but put the 30-year rate under 6% for the rest of 2026 and 2027. For 2026, Fannie Mae forecast the mortgage rate will hit 5.9% in Q2, 5.8% in Q3, and 5.7% in Q4.

Fannie Mae's expectations for slower GDP growth indicate a weaker economy in the next couple of years, and in this case, mortgage rates would go down. The March Economic Forecast also put the 10-year Treasury yield lower than the February Forecast. The 30-year fixed mortgage rate follows the 10-year yield more closely than any other index, so a lower yield would likely translate to home loan rate decreases.

Inflation has slowed significantly, approaching the Fed's 2% target; the labor market is cooling, reducing pressure on wages and prices; consumer spending has declined, signaling slower economic growth; and the Fed is expected to cut rates in mid-to-late 2026 if current trends continue.

Still, experts urge realistic expectations. While many hope for a return to the ultra-low rates of 2020 and 2021, most experts agree that rates are unlikely to fall below 5% in the near future. Most economists expect 5% to 6% to be the new normal.

The takeaway: rates are likely heading lower through 2026, but the ride will not be a straight line down.

Texas Has Its Own Rules: The Cash-Out Refinance Factor

One thing that sets Texas apart from virtually every other state is how cash-out refinancing works here.

Texas places strict requirements on cash-out refinances under Article XVI, Section 50(a)(6) of the state constitution. Because of these requirements, you will sometimes hear Texas cash-out refinances referred to as "Texas A6 refinances." Cash-out refinances in Texas are capped at 80% loan to value, meaning you will need to keep at least 20% of your home's equity.

That 80% LTV cap is a firm ceiling, not a guideline. Before you count on tapping your equity, run the numbers on your current home value and remaining loan balance to confirm you qualify.

For homeowners who simply want a lower rate or a shorter term, a rate-and-term refinance carries none of those restrictions. Refinancing can help you lower your rate or pay off your loan faster. One common type is a rate-and-term refinance, which replaces an existing mortgage with a new loan and can help you take advantage of lower interest rates or change your loan terms to pay off your mortgage faster.

What Drives Your Personal Texas Refinance Rate

The rate you see in a headline and the rate you actually qualify for are two different numbers. Several factors determine where you land.

The best Texas refinance rates are usually available to borrowers with strong credit and substantial equity. Specifically, a score of 720 or higher and a debt-to-income ratio below 43% unlock the best rates; small improvements can shave off significant basis points.

Beyond credit, your loan-to-value (LTV) ratio also affects your rate. Having more equity usually means better terms.

On the cost side, do not overlook what closing costs will do to your math. Closing costs typically run 2% to 5% of your loan amount, including appraisal, title, and origination. Divide total closing costs by your monthly savings to find how many months it takes to recoup fees and start profiting.

Shortening your term, such as from 30 to 15 years, boosts equity build-up but increases payments, so balance your goals and cash flow.

Five Moves That Put You in the Best Position

1. Get quotes from multiple lenders. Reach out to at least two to three mortgage lenders for your refinance loan to ensure you get the best rate and pricing. Rates and fees vary more than most borrowers expect.

2. Compare APR, not just the interest rate. The interest rate and APR are not the same. The interest rate affects your monthly principal and interest payment, while the APR includes certain fees. The APR is the real cost of the loan.

3. Know your credit before you apply. Before you start shopping, work on your credit score. You can check your credit report for free once each week through annualcreditreport.com.

4. Watch economic signals, not just rate headlines. Stay informed about economic trends that could indicate shifts in interest rates, helping you choose the best time to refinance.

5. Lock when the number works for you. Rate locks help provide stability by holding a specific interest rate for a set period during the buying process. A rate float-down option allows buyers to take advantage of lower rates if they drop after a rate lock.

The Texas Property Tax Reality

One factor that makes refinancing especially meaningful in Texas is the state's property tax burden. Texas has some of the highest property tax rates in the U.S. The average effective property tax rate in Texas is 1.69%, the seventh-highest rate in the country. When your total monthly housing cost already carries a heavy tax load, even a modest reduction in your mortgage rate can deliver real relief to your monthly budget.

On the upside, Texas does not have real estate transfer taxes, which are taxes imposed on the transfer of the title to real estate property. That means you will not owe extra taxes when it comes time to sell your home.

The Window Is Open. How Long It Stays That Way Is Uncertain.

The current environment is genuinely compelling for Texas homeowners who locked in rates above 6.5% over the past two to three years. Rates have pulled back from the painful 2023 highs, forecasts point to continued, if gradual, declines through the rest of 2026, and the Fed's own projections still include at least one more cut before year-end.

But the picture is not without risk. Geopolitical tensions, stubborn inflation, and shifting Fed guidance could slow or reverse that downward trajectory. Buyers and refinancers should be cautious if trying to time the market. After all, unexpected economic indicators and geopolitical events could easily disrupt any well-reasoned projection.

The smartest move is not to wait for a perfect rate that may never arrive. Run your break-even numbers today, compare offers from at least three lenders, and make a decision grounded in your own financial timeline, not a forecast.

Ready to see what your Texas refinance rate looks like today? Check your rate with Ralo now.

Related Articles

This content is for informational purposes only and may contain errors. Please contact us to verify important details.